The sharing economy has reshaped the way we live, work, and get around. Services like Airbnb have changed how we vacation. Similarly, platforms like Uber and Lyft have transformed how we think about getting from point A to point B. Among these shifts, car-sharing platforms such as Zipcar, Turo, and Getaround have revolutionized car ownership. One of those shifts is allowing individuals to use vehicles without the baggage of long-term ownership. But as the saying goes, with great convenience comes great responsibility, or in this case, the need for the right kind of insurance.

Enter non-owner car insurance. Whether you’re borrowing a friend’s car for the weekend, renting a car occasionally, or frequently using car-sharing services, non-owner car insurance can provide critical protection. But is it the right fit for your needs? This guide explores what non-owner car insurance is, its benefits and limitations, and how it works for car-sharing users. By the end of this article, you’ll have the insights you need to decide if it’s worth adding to your portfolio of protections.

What Is Non-Owner Car Insurance?

Non-owner car insurance is a specialized type of coverage designed for individuals who drive but don’t own a vehicle, particularly car-sharing users. It provides liability protection, covering injury and property damage costs if you’re responsible for an accident. This prevents you from paying out of pocket for damages, but it doesn’t offer the full protection of a standard auto insurance policy.

Unlike traditional car insurance, which is tied to a specific vehicle, non-owner insurance protects the driver. This means you’re covered no matter what car you’re driving, whether it’s rented, borrowed, or part of a car-sharing service. However, coverage options and requirements vary by state, so it’s important to check local regulations before purchasing a policy.

Benefits of Non-Owner Car Insurance

Non-owner car insurance offers several key advantages, making it a smart choice for frequent renters, car-sharing users, or those who need continuous coverage.

Here’s why this insurance policy is beneficial:

- Liability Protection: This covers the cost of injuries or property damage you may cause in an accident.

- Peace of Mind: Provides reassurance when borrowing or renting a vehicle, using car-sharing service, and ensuring you’re protected in case of an incident.

- Legal Compliance: Most states require drivers to maintain insurance coverage, even if they don’t own a car. Non-owner policies help you meet these requirements and avoid potential fines or penalties.

- Asset Protection: Helps shield your personal finances by covering liability expenses, reducing the risk of out-of-pocket costs after an accident.

What Does Non-Owner Car Insurance Cover?

Unlike traditional auto insurance, which is tied to a specific vehicle, non-owner car insurance is designed to protect the driver and not a specific vehicle. It functions similarly to liability coverage on a standard policy, covering bodily injury and property damage if you’re responsible for an accident while driving a car you don’t own; especially if you are a car-sharing user.

Depending on your insurance provider and state, your policy may also include additional coverage options, such as:

Uninsured and Underinsured Motorist Coverage

If another driver hits you and lacks sufficient insurance (or has none at all), this coverage covers your bodily injury and property damage. Some policies may include cover for lost wages, medical expenses, and other injury-related costs.

Medical Payments (MedPay) or Personal Injury Protection (PIP)

MedPay covers medical treatment for you and your passengers after an accident. PIP goes further by covering injury-related expenses, including lost income and rehabilitation costs, regardless of who caused the crash.

What Is Not Covered by Non-Owner Car Insurance?

Non-owner car insurance provides drivers essential liability coverage, but it has several key exclusions. Here’s what won’t be covered under this type of policy:

Damage to the Car You are Driving

Non-owner car insurance does not include collision or comprehensive coverage. This means it won’t cover:

- Accidents that damage the car-shared, borrowed, or rented vehicle.

- Theft, vandalism, fire, floods, hail, or falling objects.

- Collisions with animals or riots.

If the car is damaged while you’re driving, the vehicle’s owner can file a claim under their collision and comprehensive insurance, or the at-fault driver’s liability insurance (if applicable).

Injuries You Suffer in a Car Accident

Unless you add medical payments coverage (MedPay), a non-owner policy won’t cover your own injuries from a car accident. You would need additional coverage, such as personal injury protection (PIP), depending on your state’s requirements.

Other Car-Sharing Drivers

Non-owner car insurance only covers you, not your spouse or other car-sharing users in your household. Some insurers won’t even issue a non-owner policy if someone in your household already has a personal auto insurance policy.

Business Use of a Car

If you drive a borrowed or rented vehicle for work-related purposes, your non-owner policy probably won’t cover you. Business driving often requires a commercial auto insurance policy.

Personal Belongings

If your personal belongings, such as a laptop, phone, or other valuables, are stolen from a car-shared, borrowed, or rented vehicle, they won’t be covered by non-owner insurance. However, you may need to purchase additional homeowners or renters insurance to protect your personal belongings.

How Does Non-owner Car Insurance Work for Car-Sharing Users?

Non-owner car insurance works much like a standard liability policy. Car-sharing services typically include some level of insurance for users, but coverage can be limited.

If you cause an accident while using a shared vehicle and the cost of damages exceeds the service’s policy limits, your non-owner insurance can step in to cover the remaining costs, up to your policy’s limit. This ensures you are not left with unexpected expenses.

Imagine you are using a car-sharing service or driving a friend’s car and crashing into another driver’s car. The accident was your fault and it resulted in $30,000 in damage to the other vehicle. If a car-sharing service’s insurance only covers up to $20,000, you would normally be responsible for paying the remaining $10,000 out of pocket. But if you have a non-owner policy with $50,000 in property damage liability coverage, it will cover the remaining balance.

When Non-Owner Car Insurance Makes Sense

Not everyone requires a non-owner car policy, but it is suitable for certain scenarios. Here are some common circumstances where purchasing non-owner car insurance makes sense:

You Use Car-Sharing Services

Car-sharing platforms like Zipcar and Turo provide insurance coverage, but they typically only meet the state’s minimum liability requirements. In the event of a serious accident, damages and medical costs could easily exceed these limits, leaving you financially responsible for the remaining expenses.

A non-owner car insurance policy can serve as a safety net by offering additional liability coverage beyond what the car-sharing service provides. This extra protection ensures that you won’t be left paying out-of-pocket for damages or legal claims if an accident occurs.

You Regularly Borrow Cars From Others.

If you regularly borrow cars from friends or acquaintances, a non-owner car insurance policy can provide peace of mind. This coverage ensures you’re protected every time you drive, eliminating concerns about whether the car owner’s insurance will cover you or if their liability limits are too low.

NOTE: If the car you frequently borrow is owned by someone you live with, you may need to be added to their policy instead. In such cases, a non-owner policy may not cover damages from an accident. It’s best to check with the insurer to ensure you’re adequately protected.

You Frequently Rent Cars

If you rent cars often, a non-owner car insurance policy can be a cost-effective alternative to purchasing rental car insurance repeatedly. Rental company insurance typically costs at least $20 per day, meaning that if you rent for more than 42 days a year, an annual non-owner policy would likely be the more affordable option.

Just make sure to:

- Confirm that your non-owner insurance covers you in a rental.

- Check if your credit card’s rental car insurance offers coverage for rental vehicle damage. If not, you may want to consider a collision damage waiver from the rental company.

NOTE: Credit card rental insurance only applies to damage to the rental car, not liability for injuries or property damage. Combining it with the liability coverage of a non-owner policy ensures the most comprehensive protection, besides carrying an insurance policy for a car you own.

When You Are Between Cars but Want to Stay Insured

Insurance companies typically raise rates for drivers who have had a lapse in coverage even if they weren’t driving during that time. Any gap, no matter how short, can label you as a higher-risk driver, making it harder to qualify for the best rates when you need insurance again.

Since non-owner car insurance is more affordable than a standard auto policy, it’s a cost-effective way to maintain continuous coverage. When you eventually buy another car, you’ll likely get better rates than if you had let your insurance lapse.

You Need Non-Owner SR-22 (or FR-44) Insurance

An SR-22 is not an insurance type; instead, it’s only a form saying that you have insurance coverage. This is often required to reinstate your driver’s license if you are caught driving without auto insurance, get a DUI, or have another serious traffic violation. If you don’t own a car, a non-owner SR-22 policy can help you fulfill this requirement while keeping costs lower than a standard auto insurance policy.

Once you secure a non-owner policy, your insurance provider will file the SR-22 on your behalf, so you can move toward license reinstatement. While needing an SR-22 generally means higher premiums, non-owner coverage remains one of the most affordable ways to stay insured.

NOTE: Not all insurance companies offer SR-22 or FR-44 filings, especially smaller providers. If your current insurer doesn’t provide this service, you will need to find one that does to ensure compliance with state requirements.

When Non-Owner Car Insurance Doesn’t Make Sense

Non-owner insurance policies aren’t necessary for all drivers and situations. Non-owner auto insurance may not make sense if:

You Own a Car or Live with Someone Who Does

If you own a car, a non-owner policy isn’t necessary since your standard auto insurance already provides liability coverage when you borrow or rent a car. However, it’s always a good idea to check with your insurer for any exclusions or limitations. If you’re looking for additional liability protection, an umbrella policy is a better option than a non-owner policy.

If you don’t own a car but frequently borrow one from a household member, such as a parent, spouse, or roommate, you should be added to their auto insurance policy instead. Most insurers require all licensed drivers in a household to be listed on the policy, even if they only use the car occasionally. Failing to disclose this could result in denied coverage if you’re in an accident.

You Rarely Borrow Anyone’s Car

If you only drive occasionally and always with the owner’s permission, you likely don’t need a non-owner policy. In most cases, the car owner’s insurance serves as the primary coverage, meaning it will cover damages if you’re involved in an accident.

However, there are a few important considerations:

- If a claim is filed, the car owner’s insurance rates may increase, even though you were the one that caused the accident.

- If damages exceed the owner’s coverage limits, you could be responsible for paying the difference.

- Not all insurers automatically cover non-owners driving their policyholder’s car. Before borrowing a car, confirm that the owner’s insurance will cover you in case of an accident.

You Drive a Company Car.

If you regularly drive a company-owned vehicle, whether you need non-owner insurance depends on how you use the car. For instance, for business use, your employer’s insurance policy typically covers any damages in the event of an accident.

However, for personal use, the company’s insurance may not apply. If you frequently use a work vehicle for non-business activities, you may need a non-owner policy to ensure you’re covered.

Before assuming you’re protected, check with your employer about their policy’s coverage limitations for personal driving.

How Much Does Non-Owner Car Insurance Cost?

Non-owner car insurance is generally 5% to 15% cheaper than a standard auto policy with similar coverage. The savings can be even greater when compared to a full-coverage policy or insuring a high-value vehicle.

The cost of such policies varies based on factors like coverage limits, driving history, location, and how often you expect to drive. On average, non-owner car insurance costs around $438 per year.

Since premiums also differ between insurers, comparing quotes from multiple providers is the best way to find an affordable policy that meets your needs and specific situation.

If you need SR-22 insurance due to a DUI or another driving violation, expect higher rates. However, choosing a non-owner policy can still be a cost-effective way to maintain coverage and avoid lapses in insurance.

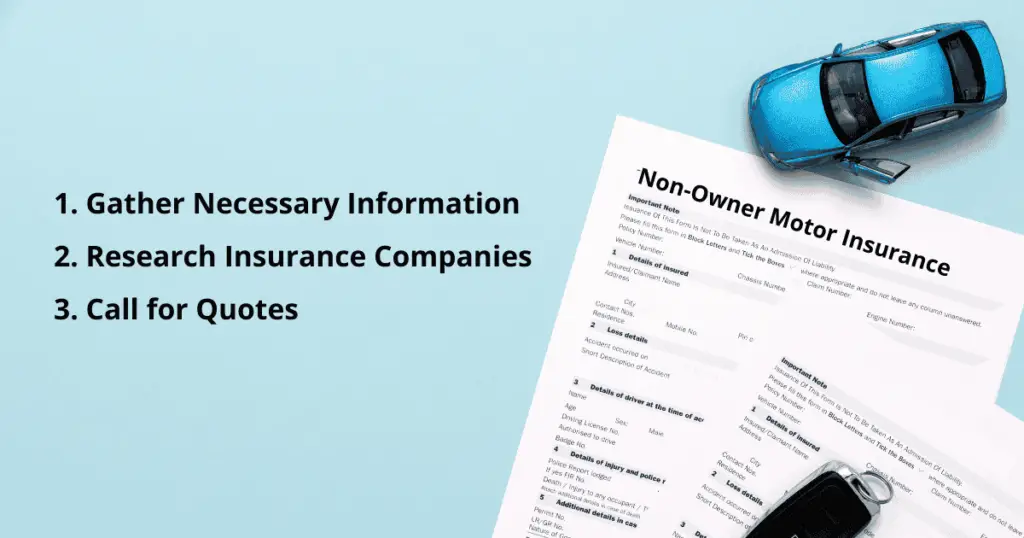

How to Get Non-Owner Insurance

Getting a non-owner car insurance policy is a straightforward process that’s very similar to purchasing a standard auto policy. You only need to follow the below steps:

Step 1: Gather Necessary Information

Before you start shopping for non-owner car insurance, it’s important to gather all the information that insurers will need. This typically includes your name, address, contact details, driver’s license number, Social Security number, and any details about past accidents or violations.

Additionally, you’ll need to know the coverage limits you want and have your preferred method of payment, such as a credit card, ready.

Step 2: Research Insurance Companies

Once you have all the required information, your next step is to research companies that offer non-owner insurance policies. Not every insurer provides this type of coverage, so you’ll need to find one that does.

It’s also a good idea to check the company’s customer satisfaction ratings to ensure you choose a reliable provider.

Step 3: Call for Quotes

Most insurance companies don’t allow online quoting for non-owner policies, so you’ll need to call the carriers you’ve identified. Be sure to have the information you gathered in step 1 on hand, as it will help you get an accurate quote.

Take the time to understand what is and isn’t covered, and ask about any additional options or features that could be beneficial for your needs.

Step 4: Compare Policies and Make Your Purchase

After obtaining quotes from at least three different insurance providers, compare their policies based on coverage, price, and overall reliability. While cost is important, it shouldn’t be the only factor you consider. Look for the policy that provides the best combination of coverage and value.

Once you have found the policy that suits you, the insurance agent will be able to take your information and get you insured. Be sure to keep your insurance documents accessible in case you need them later.

Why Non-Owner Car Insurance Is Worth Considering

The sharing economy has given us flexibility and freedom, but it’s also introduced new complexities, especially when it comes to insurance. Non-owner car insurance is an affordable, straightforward way for occasional drivers and car-sharers to ensure they’re covered. With liability protection and cost savings as key benefits, it aligns with the needs of today’s on-demand lifestyle.

If you regularly borrow cars or use platforms like Zipcar and Turo, understanding your insurance options is essential. Take charge of your financial and personal well-being by exploring non-owner car insurance today!