If you’re looking for a safer way to pay bills or transfer money without using cash or a bank account, a money order might be just what you need. With a money order, there is no need to worry about checks or waiting for one to clear. Simply purchase a money order at a local store and send it to the recipient.

This guide will break down everything you need to know about money orders, including how they work, their advantages, and situations where they come in handy. By the end, you’ll feel confident about whether a money order is the right financial tool for you.

Money Order Overview

A money order is a secure, prepaid, paper form of payment that works similarly to a personal check but with key differences and features. Unlike checks, which rely on available funds in a bank account, money orders are paid for upfront using a debit card, cash, or a traveler’s check. This guarantees payment and eliminates the risk of a bounced check due to insufficient funds. However, money orders typically have a maximum limit of $1,000.

One of the main advantages of a money order is security. Only the designated recipient (the person or business named on it) can cash or deposit it. This makes money orders a safer alternative to carrying cash.

Money orders are widely available for purchase at banks, post offices, supermarkets, and convenience stores. Many of these locations also offer cashing services, allowing both buyers and recipients to use money orders without needing a bank account.

Common Uses of Money Orders

- Paying Bills: Money orders provide a reliable way to pay bills, especially for individuals who prefer not to use electronic payments or lack a checking account. Many landlords, utility companies, and service providers accept them as a valid payment method.

- Making Purchases: Some sellers, particularly those in online marketplaces or businesses dealing with high-ticket items like furniture or appliances, require guaranteed payments. In such cases, money orders serve as a secure alternative to cash or personal checks.

- Sending Money Abroad: Since money orders are accepted in many countries, they are a popular option for international remittances. Just remember that international money orders often come with higher fees.

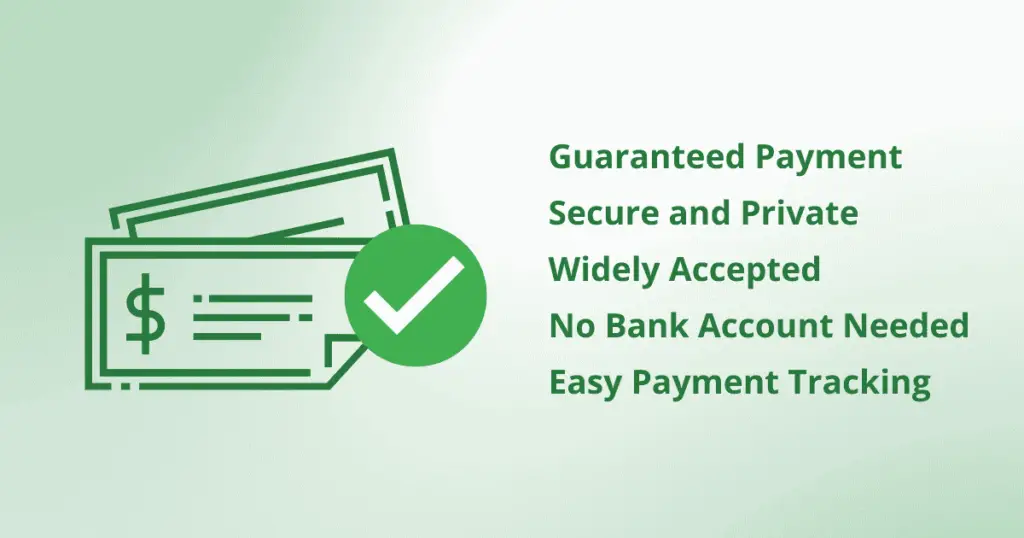

Advantages: Why You Should Use a Money Order

Money orders offer several benefits, making them a preferred payment method for many people. Here’s why they might be the right choice for you:

Guaranteed Payment

Unlike personal checks, which can bounce if there are insufficient funds in the account, money orders are prepaid. With a money order, funds are already set aside and available when the recipient cashes it.

Secure and Private

Money orders are usually safer than personal checks since you can purchase or cash a money order without including your sensitive personal bank details. Checks have your bank account number printed on the front, exposing pretty vital information to would-be criminals. The additional layer of privacy reduces the risk of identity theft and fraud.

Widely Accepted

Money orders are accepted at many many businesses, including banks, utility providers, and some retail stores. This makes them a convenient payment option, especially in situations where checks or credit cards are not accepted. They are also appropriate for both domestic and international payments.

No Bank Account Needed

The great thing about money orders is that you don’t need a checking or savings bank account to buy or cash a money order. You can even pay with cash, making it a great alternative for those without access to traditional banking services.

Easy Payment Tracking

When you purchase a money order, you receive a receipt with tracking information. This allows you to check the status of the money order to verify if it has been cashed, providing peace of mind and proof that it was received.

Potential Drawbacks and Cons of Money Orders

While money orders offer security and convenience, they also have some limitations to consider:

Limited Transaction Amounts

Typically, money orders have a maximum value of $1,000, making them impractical for larger purchases or payments. If you need to send more, you may have to buy multiple money orders, which can be inconvenient.

Fees Can Add Up

Purchasing a money order usually comes with a small fee, usually between $1 and $5 for domestic transactions. International money orders may cost more. The recipient may also need to pay a fee to cash it.

While these fees might seem minor, they can quickly add up, especially for frequent users. That is especially true if you pay multiple bills per month with money orders.

Slower Than Digital Payments

Money orders need to be physically delivered or mailed. This may take longer to reach the recipient compared to electronic payment methods, which are almost instant.

Less Convenient to Purchase

Unlike digital payments, which can be made from a phone or computer, buying a money order requires a trip to a bank, post office, or retail location. This extra step is often less convenient and time-consuming.

Risk of Loss or Theft

Although money orders are safer than carrying cash, they can still be lost or stolen. Replacing a lost money order can be a lengthy process and may involve additional fees.

To avoid additional headaches, always tear off and keep the receipt portion of the money order before you send it. In the event a money order is lost it will be much easier to get new ones printed if you have the receipt.

How Do Money Orders Work?

Money orders work similarly to personal checks, providing a secure way to make payments. The buyer purchases a money order and gives it to the recipient, who can then cash it at a bank, deposit it into their bank account, or take it to a location that chases money orders.

In fact, the main difference is that a money order is guaranteed since you pay with cash or an instant debit card transaction. In contrast, when writing a check, money does not come out of your account until the recipient deposits it into their bank account. Now, let’s take a closer look at how money orders work.

Step 1: Purchase a Money Order

Buying a money order is simple. Start by finding a location or place that sells money orders. Fortunately, you can find money orders at various locations, including:

- The United States Postal Service offices

- Payday lenders

- Convenience stores

- Check cashing service providers

- Grocery store customer service counters

- Money services or customer service counters at major retail stores

At the counter, inform the cashier you want a money order and specify the dollar amount you need. Be prepared to pay the full amount upfront using cash or a debit card. Keep in mind that you will be required to pay for any fee that may apply and you cannot pay with a credit card.

Step 2: Fill Out the Money Order

Money orders may appear different depending on where you purchase them. But generally, filling one out is similar to filling out a personal check. It comes dated and with the amount printed on it. You fill out the following information to ensure it reaches the right person.

- The recipient’s name and address. This ensures that only the intended business or person can cash it

- Your name and address as the buyer

- A memo or note (optional) to specify the purpose of the payment. This may include information like an invoice number so the payment is applied to the proper bill.

Step 3: Keep Track of Your Money Order

After purchasing the money order, keep your receipt in a safe place. It usually contains a tracking number or other code that allows you to monitor its status and confirm the payment’s delivery, or request a replacement if it’s lost or stolen.

Be sure to tear off the receipt portion of the money order before mailing it out. Keep the stub in a safe place for your records in case you need it later.

Step 4: Cash or Deposit the Money Order

If you are the recipient of a money order, you have two options: cash it or deposit it into your bank account.

- Cashing a money order: To avoid extra fees, try cashing the money order at the location that issued it. For instance, the United States Postal Service allows you to cash its money orders for free at any post office. If you choose to cash it at a check-cashing store or a third-party service, you may be charged a fee.

- Depositing a money order: Many banks and credit unions allow you to deposit money orders, just like a regular check. In some cases, you may be required to visit a physical branch instead of using an ATM or mobile deposit.

Before deciding how to cash or deposit your money order, check with the issuing provider and your bank to understand any applicable fees or restrictions.

When Should You Use a Money Order

With so many ways to send and receive money, checks, online apps, and cash, you might wonder when a money order is the best option. Here are some situations where a money order can be useful:

When You Don’t Have a Bank Account

If you don’t have a bank account or access to paper checks, a money order can serve as a secure alternative as you pay for a money order with cash. Since a money order allows you to cash without needing a bank account, there are no risks of it bouncing like a check. But keep in mind that money orders usually come with a small fee.

When sending payments through the mail

Unlike cash, money orders can only be used by the intended recipient. And unlike personal checks, they don’t include sensitive banking details like routing numbers and personal account information. This makes them a safer choice for those sending money through the mail.

When You Need Immediate Payment

Waiting for a check to clear can be frustrating, especially if you need quick access to funds. If depositing into a bank account, you may still need to wait a few days, but it’s often faster than processing a check.

Money orders can eliminate that delay. If you’re cashing one, you may be able to receive the money immediately since it is a secured form of payment.

When Should You Not Use a Money Order?

While money orders offer security and convenience, there are times when they may not be the best option:

- When making large transactions: Most money orders are capped at $1,000. If you need to send a larger amount, a cashier’s check or wire transfer may be a better option.

- When speed is essential: Money orders require physical delivery, whether by mail or in person. If you need instant payment, digital transfers or peer-to-peer apps like Zelle, Venmo, or PayPal are much faster.

- When making online purchases from unknown sellers: Scammers may ask for money orders as they are difficult to trace or cancel once sent. If you’re making an online purchase, consider using a credit card for added fraud protection.

- When you want interest or rewards on transactions: Unlike a credit card or bank account, money orders don’t offer rewards, interest, or cashback on transactions.

- When paying businesses or individuals that prefer electronic payment methods: Some businesses no longer accept money orders, favoring electronic payments for convenience and security.

Money Order Alternatives

A money order is not the right payment option for every need. Consider factors such as processing speed, fees, and how easily the recipient can access the funds when looking for an alternative. Here are some of the best alternatives to consider:

1. Cashier’s Check

A cashier’s check is a secure payment method issued by a bank or credit union, with funds taken directly from your account. Cashier checks are guaranteed by the bank, making them ideal for larger transactions where cash or personal checks might not be accepted. They are issued and signed by a bank representative, meaning they are widely trusted and considered safe.

2. Wire Transfer

A wire transfer is an electronic transfer of funds between banks, credit unions, or financial service companies. This method allows individuals or businesses to send money quickly without using cash or checks. You’ll need to provide the recipient’s name and banking details and pay a fee upfront.

- Processing time: Domestic wire transfers typically take 1–3 business days, while international transfers may take 2–5 business days.

- Fees: Banks usually charge a fee for both sending and receiving wire transfers, which can be expensive.

3. ACH Transfer

An ACH (Automated Clearing House) transfer is another form of electronic payment used for direct deposits, recurring bill payments, and other online transactions. Unlike wire transfers, ACH transfers are processed in batches and may take longer (1–3 business days), but they are often free or low-cost.

Transfers such as payroll direct deposits and online bill payments commonly use ACH transfers.

4. Digital Payment Services

Digital payment Apps like Zelle®, Cash App, and PayPal provide a fast and convenient way to transfer money or make payments electronically. These services allow users to transfer funds instantly, often without fees, as long as both parties have an account with the platform.

Final Thoughts: Is a Money Order Right for You?

Money orders remain a dependable and accessible payment method, offering security, affordability, and flexibility, especially for the financially underserved. Whether you’re paying rent, managing your budget without a bank account, or ensuring timely bill payments, money orders can simplify your financial life.

However, they aren’t the best fit for every scenario. If you’re sending large sums or need fast payment options, you might want to explore other methods like wire transfers or cashier’s checks.

For those considering money orders, they can be a practical, user-friendly solution. Evaluate your financial needs and use tools like money orders wisely to stay in control of your money and transactions.